The Silver Squeeze is Working – Part II

The Silver Squeeze is Working – Part II

“Conspiracy theorists of the world, believers in the hidden hands of the Rothschilds and the Masons and the Illuminati, we skeptics owe you an apology. You were right. The players may be a little different, but your basic premise is correct: The world is a rigged game.” – Matt Taibbi

I hate the phrase “conspiracy theorist,” although I’ll use it a few times in this piece. I suspect few people understand how it was born into our cultural lexicon or how damaging it is to a free and open society. Briefly, it was concocted in the aftermath of the Kennedy assassination as part of an overt disinformation campaign to quell a growing intellectual rebellion on the domestic front. Odd that such a thing was needed, to be sure.

The phrase is meant to denigrate and shut down open debate. As such, it is a powerful tool of propaganda. There’s a strong natural desire for humans to be included in the tribe, you see, and in case you are wondering, tribal leaders usually have a firm No Tin Foil policy. Oswald did it and he acted alone! We actually landed on the moon! The Roswell crash was a weather balloon! The amount of gold and silver we claim are in the vaults is actually there!

Record scratch. About that last point…

There are actually two conspiracy theories widely proposed (and often co-mingled) by the precious metals crowd. The first is that the official precious metals vaults (COMEX, London Bullion Market Association (LBMA), etc.) don’t have the gold and silver they claim to hold. The second is that the big banks collude to suppress the price of gold and silver via the futures market on behalf of the Bank for International Settlements (BIS), aka the bank for central banks. As a card-carrying member of the precious metals crowd, I’m a believer in the second but dubious on the first. Well, more specifically, I don’t think the first has to be true in order for the second to be true, and the second is way more important. They are essentially unconnected conspiracies.

I should say upfront that I personally don’t think it’s a scandal or even a big deal that open interest in silver and gold futures contracts exceeds the amount held in vaults (by a wide margin, no less). It is a feature of futures contracts. It allows for liquidity and simplifies life for hedgers, speculators and market makers alike. Take lean hog futures as an example. A contract represents 40,000 pounds of lean hogs, settled by cash. If you wanted to acquire 40,000 pounds of lean hogs, buying a futures contract and trying to stand for delivery wouldn’t work. Not only would it really annoy your neighbors, but you also aren’t allowed to anyway since the contract only settles for cash (you accept cash if the price of lean hogs goes your way, pay cash if it doesn’t). So why have the contract at all? It turns out all kinds of commercial transactions between private parties are benchmarked to that contract, customized for their own particular needs, and the contract provides a standardized instrument that facilitates an efficient pork market. As a chicken, I’m all for it.

Of course, in their own ways gold and silver are different from other commodities (and from each other). Gold has a been money for millennia because of certain chemical and physical properties. It is durable, infinitely and easily divisible, and highly inert – it rarely exists in anything other than its metal form, it doesn’t oxidize, and so on. Precisely because of this inertness, there are few industrial applications for gold beyond jewelry. Unlike with lean hogs, people like to have direct access to their money, at least occasionally, and so standing for delivery on a gold futures contract is quite common (and, ironically, comparatively easy versus most other commodities).

Silver, on the other hand, plays a dual role in our society. It is both a monetary and an industrial metal, which complicates things a little. As a monetary metal, silver is the uncouth poor cousin to gold. Sure, it was once useful as coinage, since it has always been a lot cheaper than gold, which used to make it ideal for small, everyday transactions (before we debased our fiat currencies to the point where we had to drag nickel and copper in off the street – don’t get me started on them). But silver also tarnishes a little over time and nobody would confuse it with its Ivy League educated older cousin. As the blue-collar monetary metal, silver has to work for a living – side hustles, so to speak. One huge application for silver is in the production of solar panels. Each solar panel produced contains about 2/3rds of an ounce of silver, mainly because it is an excellent conductor. Last I checked, the Chinese are making a lot of solar panels.

With this background complete, here’s what I believe the r/Wallstreetsilver crowd is hoping to accomplish with the silver squeeze:

Remove as much physical silver from the market as possible, either by purchasing and hoarding actual physical silver from the open market (silver stacking) and/or through the purchase of PSLV

Prove the COMEX vault does not have as much silver as it claims, sparking a run on physical silver by big money types

Cause the price of silver to skyrocket as continued price suppression becomes impossible, which would bring gold along for the ride as panic buying spread to both monetary metals

Debase the US dollar as the world realizes the conspiracy theory of precious metals price suppression is a conspiracy fact

Here’s what I think is actually happening:

The r/Wallstreetsilver crowd is removing a lot of physical silver from the market

Concurrently, industrial demand for silver is spiking as the world reopens

It is becoming more difficult to suppress the price of silver and those cracks are beginning to show

Gold will do what gold does, independent of what’s happening with silver, because Harvard grads don’t take cues from the help

In The Silver Squeeze is Working – Part I, I covered the first point. I intend to cover the second and fourth points in future Doomberg essays and will focus the rest of this piece on the third.

Two significant tribal leaders in the gold and silver space are the previously mentioned LBMA and the United States Mint. In the past several weeks, both have exhibited strange behavior – strange being the kindest adjective I could come up with. As a certified doomer, strange behavior by tribal leaders triggers my spidey sense. Something big is afoot – the silver squeeze is having an impact. Let’s begin with the LBMA…

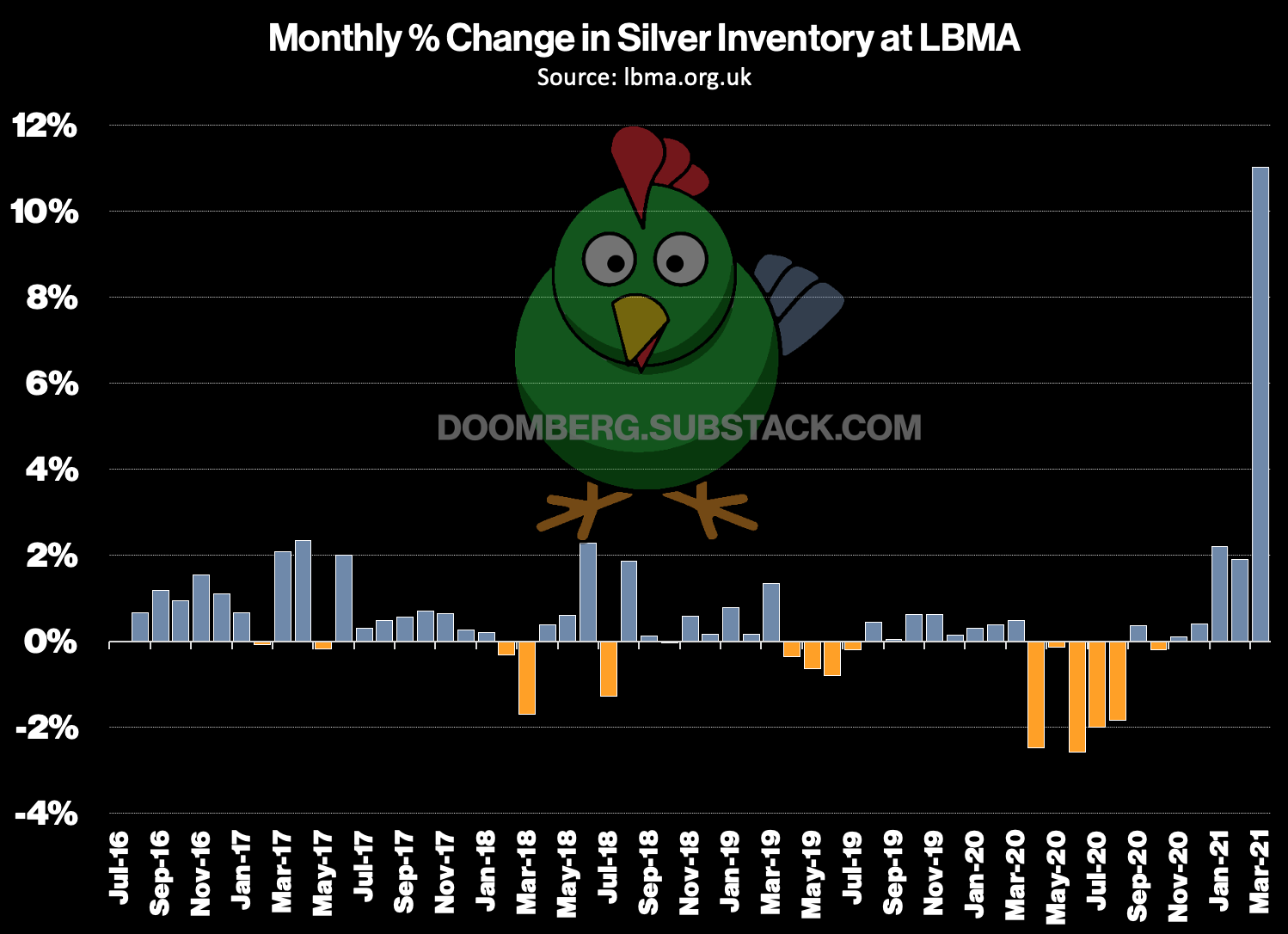

On April 9, the LBMA shocked the precious metals world by announcing total silver held in London vaults at the end of March had grown by a staggering 11% over the February total. This was, quite literally, an unbelievable figure, especially in the face of the silver squeeze. Reports from silver buyers all over the globe indicated unprecedented shortages and difficulty sourcing physical metal, but the LBMA trumpeted its biggest month of inflows on record. Just how unbelievable was the original report? Here’s a chart of the previous 55 monthly percentage change in flows along with the astounding March figure. The prior average monthly change was +0.3% with a standard deviation of +/-1%, while the largest change on record was +2.33%, reported in April of 2017.

The report served its likely intent – at least some of the air in the silver squeeze balloon was popped. Then quietly, almost as an afterthought, on May 10th the LBMA informed the world in a footnote to the April report that the real increase in March was a paltry 1.6%, not the robust 11% originally reported. They described it as a data submission error from one of the six vaults which hold silver on behalf of the LBMA.

Much outcry ensued. LBMA defenders, and even some precious metal conspiracy theorists, chalked up the “mistake” to an “accounting error.” I wrestled with the significance of this issue for several days as I thought about writing this piece. I finally settled on “knowing deception” being the motivation, but perhaps not at the LBMA specifically. Here’s why. The six LBMA London vaults are operated by JP Morgan, HSBC, Brinks, Malca-Amit, Loomis, and ICBC Standard. Little is known about the distribution of silver between these six vaults, but let’s assume as a thought experiment it is equally distributed between them (i.e., they each hold 16.67% of the LBMA total silver). The error at issue here is 11% - 1.6% = 9.4%. But! That’s the error at the LBMA level. If the silver is equally distributed, the transmission error at the one offending vault operator is actually 9.4/16.67 = 56%!! If you relax the assumption of equal distribution and assume the largest vault holds 40% of the LBMA total and this largest vault was the offender, the transmission error is still a whooping 9.4/40 = 24%. It is unfathomable that a vault operator would make a mistake like this. They are literally in the silver counting business!

Here’s my best guess. The offending vault operator was caught totally offsides by the silver squeeze and lied to the LBMA. The LBMA failed in its due diligence and was embarrassed by the outcry that followed. The lie worked, buying precious time for the offending vault operator. The LBMA insisted on correcting the record, and here we are. That’s the best I got. Before leaving this part of the story, ask yourself this: Would an error showing an erroneous 11% outflow from the LBMA vaults in the middle of the silver squeeze have been printed without double and triple checking? I think not. There’s your answer. Knowing deception, it is.

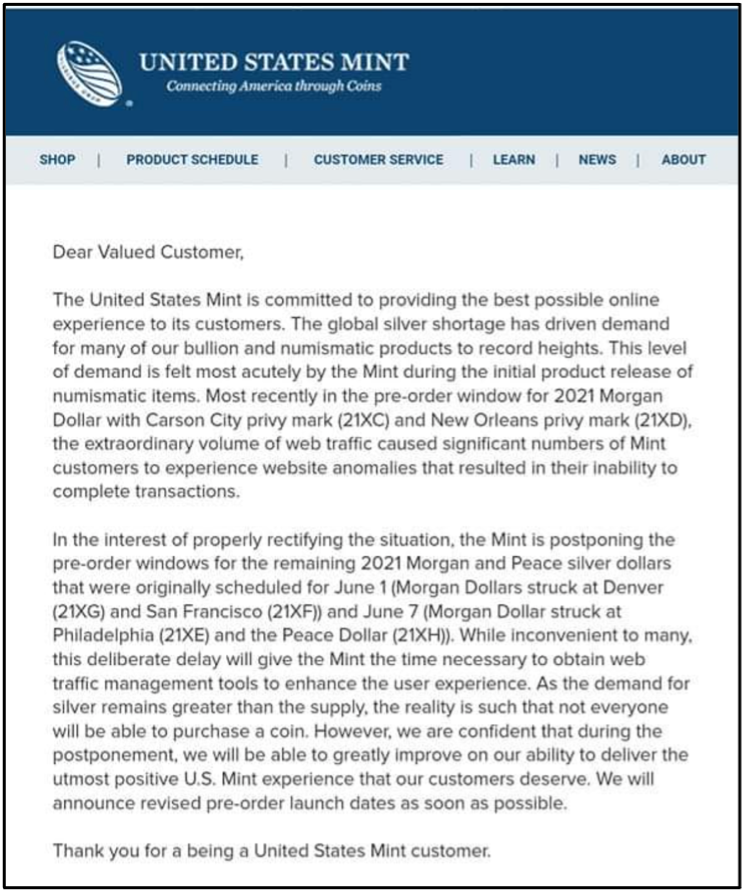

On to my favorite development of the past few weeks. On May 28th, the venerable United States Mint sent an email to customers and the industry press that can only be described as baffling:

Here are the key passages:

“The global silver shortage has driven demand for many of our bullion and numismatic products to record heights.”

“As the demand for silver remains greater than supply, the reality is such that not everyone will be able to purchase a coin.”

So much to unpack here. First, shortages don’t create demand – it’s the other way around. It’s bizarre that the United States Mint would flub this basic rule of economics. Second, and more critically, what silver shortage? According to the LBMA and COMEX, there’s (literally) tons of silver available for delivery. Supply is abundant. Further, the price of silver has been range-bound between $23-$28 an ounce for almost a year. It is nonsensical to say the demand for silver is greater than supply because the current price is, at least in theory, always and instantaneously the precise point where supply and demand reach equilibrium. Unless for silver… it isn’t?

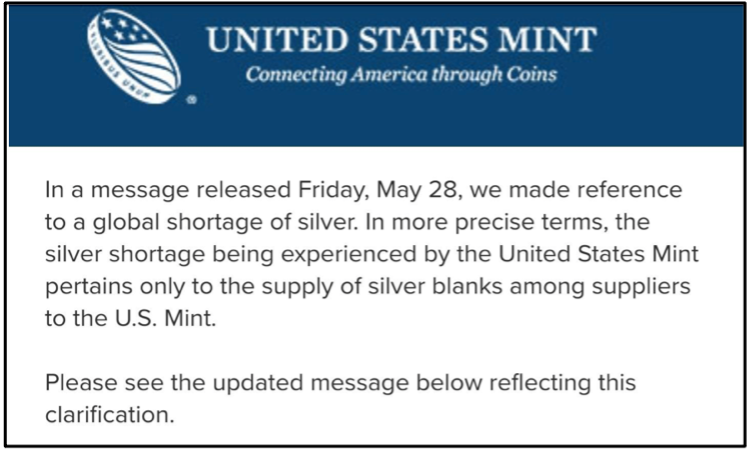

Naturally, the outcry from this announcement sent the Mint into damage control. On June 2, they issued a new statement clarifying what they allegedly meant to convey. Here’s how it starts:

Ah yes! A silver blank shortage! Yeah, that’s the ticket! Silver blanks. Got it. Never mind that the same analysis above applies to “suppliers to the U.S. Mint.” The entire affair is downright embarrassing.

What do I conclude from the strange behavior of the LBMA and United States Mint? It seems obvious to me the silver squeeze is working, demand for physical silver is skyrocketing, and the price of silver is being artificially suppressed. When the price of a desirable good is held below its natural market equilibrium value, demand will continue to chew up supply until it is exhausted or price is finally allowed to rise. If the price of lean hogs were suppressed down to $0.10 a pound, you can bet your bottom dollar demand for beef (and chickens!) would wane. Now that’s an experiment worth running!

I personally believe these dynamics are stretching silver supply chains to their breaking points and something has to give. I happen to think price is that something.

If you enjoy Doomberg, sign up yourself and share a link with your most paranoid friend!

When is the next Silver article?

Hey Doomberg, this is Jim Lewis from Wall Street Silver. Can we interview you on our YouTube channel?