Instability Coins

“His debts approached three thousand dollars and, as Ponzi liked to say, his only assets were his hopes.” - Mitchell Zuckoff

Last Friday evening when I wrote Crypto Carnage Coming?, I never could have imagined the historic events of the past few days. Carnage did indeed arrive on Wednesday, seemingly out of nowhere, when Bitcoin crashed to just above $30K – a nearly 50% haircut from the previous week’s highs – only to rip back to over $40K on the same day.

The ostensible cause of the collapse was news out of China that regulators were making moves to ban cryptocurrencies, while the apparent cause of the subsequent relief rally was, at least in part, Elon Musk’s diamond hands tweet within minutes of the bottom.

I have my doubts about both. I think something much bigger could be afoot. Indulge me as I don some tin foil. I think the entire crypto space is teetering on the edge of a total collapse that might threaten the stability of the broader financial system. Hyperbolic? Perhaps. But the sky is always falling here at Doomberg. In this essay, I dig down into the remarkable rabbit hole of stablecoins.

Before we begin, consider that if I went down to my local bank and withdrew $9,900 of my own money three times in one day, I’d most likely get a call from the Treasury’s Financial Crimes Enforcement Network. Depending on how I responded to inquiries by the authorities, I could theoretically be charged with structuring, a crime that is punishable by a prison sentence of up to five years. Mind you, it’s my own money in my own bank account, but in the real-world governments pretend to care an awful lot about money laundering.

In the crypto world? Not so much.

A stablecoin is a cryptocurrency which attempts to offer price stability because it is backed by a reserve asset (i.e., fiat currencies, precious metals, etc.). You give me the reserve asset, I’ll issue you a stablecoin, and if you ever want your reserve asset back, we’ll reverse the transaction. Don’t worry though, I’ll be sure to keep your reserve asset good and safe, lest you are concerned about the ability to have it returned to you in a timely manner. The stablecoin can then be used for all manner of trading with other crypto market participants across and between exchanges of varying sketchiness. See where I’m going here?

For our purposes, we’ll focus on a particularly important subset of stablecoins – those allegedly backed US dollars. This might come as a surprise to you, but there exist totally unregulated entities that can effectively issue US dollar equivalents in unlimited quantities. Naturally, they have.

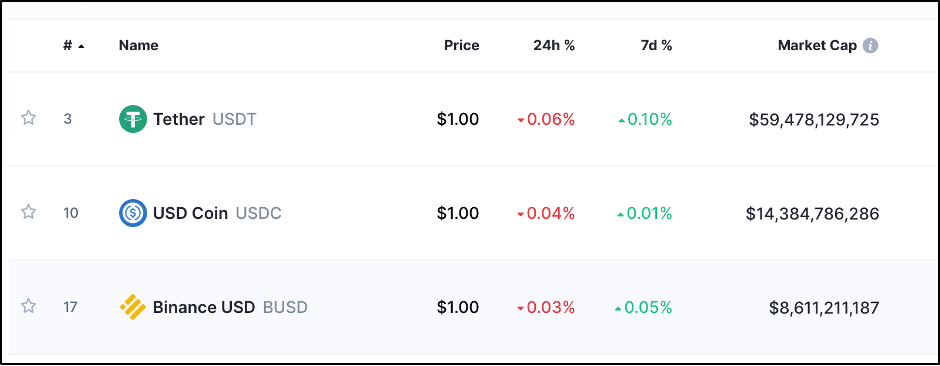

As of this writing, the top three US dollar stablecoins are Tether (symbol: USDT), USD Coin (symbol: USDC), and Binance USD (symbol: BUSD). Together, they have a market cap of over $80 billion! I pulled this data from coinmarketcap.com:

It gets better! It’s kinda sorta understood by most crypto market participants that the largest stablecoin, Tether, is most likely a fraud. That it does not, in fact, have $59+ billion of US dollar equivalents stashed away in various respectable institutions. To be clear, I’m not saying Tether is a fraud, I’m saying lots of really smart people in the crypto space operate under the assumption that it’s a fraud.

The red flags around Tether are numerous. Until recently, it had never disclosed meaningful information about its reserves. New York State Attorney General Lelitia James settled a long-standing investigation into Tether (and its closely related party Bitfinex) in February, saying this:

“Bitfinex and Tether recklessly and unlawfully covered up massive financial losses to keep their scheme going and protect their bottom lines. Tether’s claims that its virtual currency was fully backed by U.S. dollars at all times was a lie.”

A lie of this magnitude seems like a big deal. Certainly, a much bigger deal than a few $9,900 withdrawals from Bank of Middle America by yours truly. However, the terms of the settlement are a little light on punishment, if you ask me. The companies agreed to stop doing business in New York State, paid a moderate fine, admitted to no wrongdoing, and agreed to substantially more transparency going forward. Time will tell whether this is the first step toward legitimizing Tether, or the first step toward unraveling it as a fraud.

USDC, however, is another matter entirely. Widely characterized as the “good” stablecoin, USDC is run by Circle, which was co-founded by Centre and Coinbase. Coinbase, the second largest crypto exchange by volume behind Binance, recently had a successful direct listing on the Nasdaq (symbol: COIN). It currently trades with a market cap of $58 billion, although this is down about 50% from its high achieved on the first day of trading in mid-April. On the path to legitimizing cryptocurrencies, the Coinbase direct listing is a gigantic milestone. The Coinbase brand is closely tied to USDC’s brand. If USDC is something other than it is portrayed to be, things could get interesting pretty quickly.

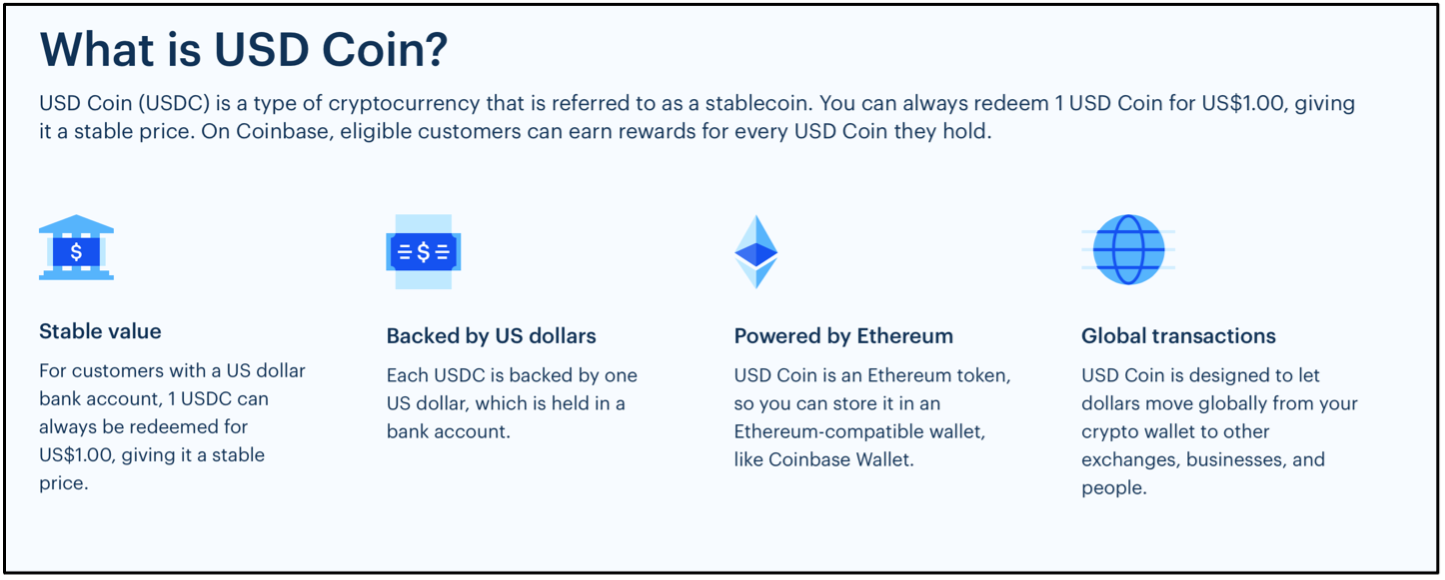

I pulled the following screenshot directly from Coinbase’s website:

Stable value. Backed by US dollars (held in a bank account, no less!). Powered by Ethereum. Global transactions. What’s not to like? That’s where my online Twitter friend @DesoGames comes into the picture. In a late-night direct message exchange, @DesoGames, a ferocious and relentless proponent of the crypto-as-fraud thesis, pointed me to a most interesting set of facts as it pertains to USDC. I credit him for the genesis of much of what follows below.

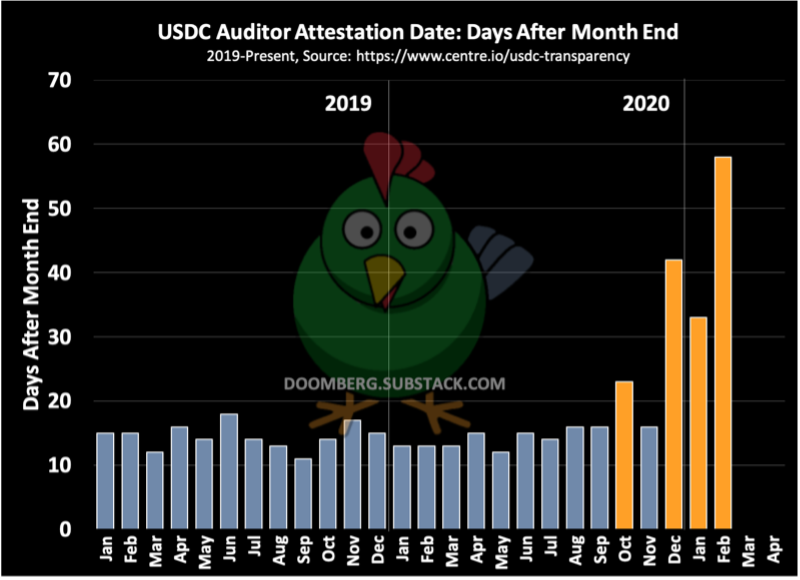

The primary reasons USDC is considered the “good” stablecoin are simple enough. First, its close association with Coinbase brings substantial positive brand coverage. Second, from the onset of USDC’s existence, Circle has released a monthly statement from a respected auditor, Grant Thornton LLP, attesting to USDC’s reserves. To be clear, an attestation from an auditor is not an audit. But it’s something. It’s a heckuva lot more than Tether has ever produced. You might not have heard of Grant Thornton LLP before reading this, but they aren’t some unknown bucket shop auditor. They are the American member firm of Grant Thornton International, the seventh largest accounting network in the world. In short, Grant Thornton LLP cares about its reputation.

Month after month, usually within two weeks of month end, Grant Thornton LLP would release its letter attesting to USDC’s growing reserves. Then something odd began to happen. Take a look at the chart below. For the month of October 2020, the attestation letter came late – 23 days after month end. November was normal enough, but then it took 42 days for the December attestation to publish. The letter for January 2021 arrived after 33 days, while February’s letter took 58 days to publish. As of this writing, there is no attestation for USDC’s reserves for March or April.

To make matters more interesting, USDC issuance has gone completely vertical. The circulating supply as of the last attestation (i.e., February 28, 2021) was $9.3B. USDC has issued an astounding 50%+ more stablecoins since then.

Is there an innocent explanation for all this? Perhaps. But consider this pattern of recent events:

APRIL 14 – Coinbase begins trading on the Nasdaq via a direct listing. Many in the media are erroneously referring to this as an IPO – it’s not. A direct listing isn’t underwritten by investment banks, typically doesn’t raise funds for the company, and comes with less disclosure obligations than a traditional IPO (i.e., no roadshows, and thus direct listings can come together more quickly). Instead, a direct listing is merely a liquidation event for founders (although it does make it easier to raise funds in the future). Insiders at Coinbase dumped massive amounts of stock into the direct listing. For example, many key officers sold nearly all of their vested shares. In total, 2iqresearch.com estimates insiders dumped $4.6B worth of Coinbase stock in the first days of trading. That’s an impressive bounty.

APRIL 27 – Circle finally publishes Grant Thornton LLP’s attestation of USDC’s February reserves. There is no explanation for the extended delay.

MAY 17 – Coinbase surprises the market by announcing it will be raising funds by issuing a convertible bond. The offering was $1.25 billion (plus another $187.5 million option granted to underwriters). Many thought it was odd that Coinbase would issue convertible debt with the stock down ~50% from the direct listing.

MAY 18 – Both Tether and USDC trade outside their normal tightly held pegs. Although not unprecedented, this is unusual. An entire universe of crypto traders usually closes these arbitrage opportunities by swiftly buying and selling stablecoins for fractionally different prices across multiple exchanges for a profit.

MAY 19 – Cryptocurrencies undergo an epic crash and partial recovery.

Maybe these are unconnected events. Maybe not. Let’s explore what it could mean if my hunch is correct.

If USDC does not have the reserves it claims it has, it is effectively a Ponzi scheme. If USDC is a Ponzi scheme, Coinbase is fatally wounded. If Coinbase is fatally wounded, it could trigger a massive collapse of the entire crypto ecosystem. Doubt me? Walk through what an unraveling of Coinbase would look like. By listing on the Nasdaq, Coinbase serves as a potentially toxic sewer pipe connecting all the chicanery of cryptocurrencies to the traditional finance world. The blowback would be astronomical.

Retail investors across the world would lose untold billions of dollars. Regulators would be outraged. Panic would ensue. Many cryptocurrencies would go no bid. Unlike traditional stock exchanges, major crypto exchanges have no circuit breakers. The fall would make Wednesday’s event seem like a warmup act. The panic would bleed into the stock market, causing a major risk-off correction.

An awful lot is riding on the March attestation of USDC’s reserves by Grant Thornton LLP. In the meantime, one can’t help but wonder if their only assets are their hopes?

If you enjoy Doomberg, email a link to your most paranoid friend!

Not sticking my neck out for Tether that case is still TBD but as I sit here today 1.5 years after you wrote this article USDC is looking rock solid. I think the thing that self professed “no coiners” often overlook with stable coins is the incredible opportunity they offer the US. Everyone wants dollars the only problem is they can’t access them. If the United States we’re to really get behind stable coins every weak currency in the world would collapse into the dollar. Secondly if they were fully regulated requiring 1 to 1 backing in US Treasury bonds it would solve another massive problem we and every other country faces ie who the hell other than our own central bank is going to buy our negative real yielding debt?

This is an interesting thesis, but its major flaw is that there has to be a catalyzing event.

For top level pyramid/Ponzi schemes - this generally involves either a legitimate law enforcement prosecution or a failure in the chain of payments.

I do not see, from the article above, any evidence of either.